The precise timing and severity of a pandemic is impossible to predict: there is no Minority Report-style “pre-pandemic”, where genetically-blessed soothsayers see the future. But as we discussed in previous posts, it is possible both to prepare for an outbreak, and to understand which scenarios will have the biggest impact on your organization.

But what about the government response? Again, our previous post discussed how this will have an even bigger financial impact on most organizations than the novel coronavirus itself – both the economically negative impact (e.g. the lockdown), and the positive (e.g. stimulus). Can at least some of that be predicted? Can we prepare for lockdowns, squillions in government aid, lockdowns being lifted and travel bubbles being inflated? As with the pandemic, no-one can predict government actions for sure. But based on their pronouncements and track record, there are some outcomes that are more probable than others.

In the “multiple scenario” approach, it’s possible to incorporate all kinds of shocks, including positive ones (government aid, stimulus packages, lower interest rates etc); and negative ones (macro and geopolitical shocks, crises in specific industries, natural disasters etc). This daily combination of positive and negative shocks has been driving equity markets higher of late. Investors have been latching on to progress with COVID-19 vaccines, and the reopening of the economy (such as this week’s record jump in U.S. retail sales), and appear confident these developments – along with government stimulus – will continue to support equities. At the same time, investors have seemingly ignored scary numbers like a 20% drop in U.S. GDP and double-digit unemployment. Equity markets have now recovered – or almost made back – all their initial losses due to the pandemic and lockdown.

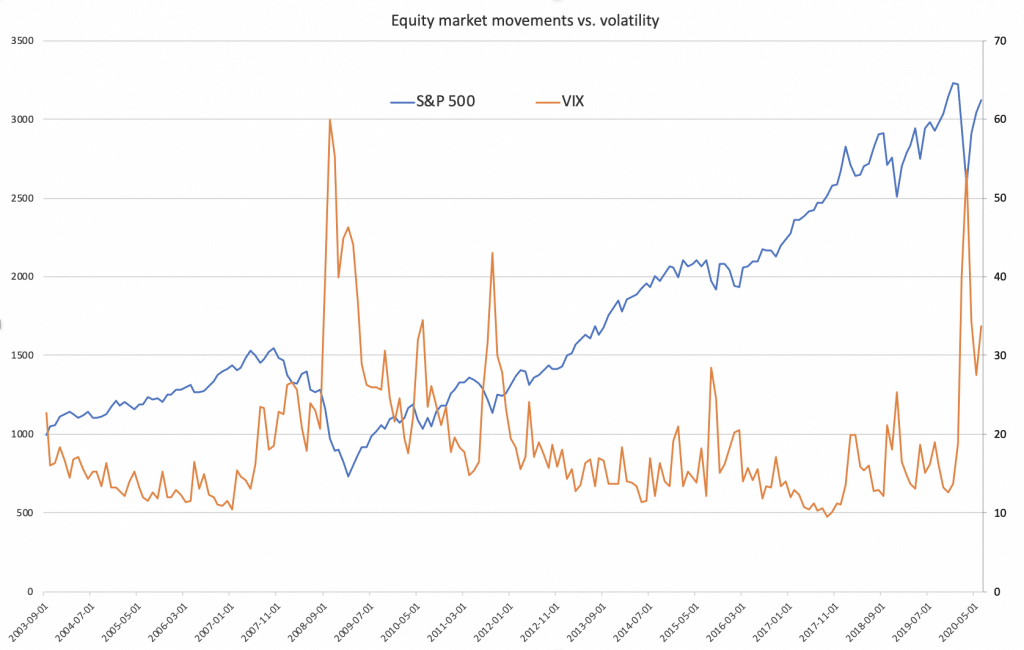

Despite this, now is not the time for complacency. Massive defaults could be just around the corner. Back in 2007, with market liquidity drying up by the summer, equity markets kept growing till November. Government stimulus and a moratorium on mortgage and some other debt payments might delay and/or soften a surge in defaults, but probably won’t be able to eliminate them altogether. It’s also worth noting the impact of negative shocks is usually higher than positive ones: an observed strong negative correlation between equity prices and their volatility supports this (see chart). If positive and negative shocks had similar effects, volatility would jump on large positive and negative swings in prices; the correlation between price and volume would be close to zero. Since we’re now observing strong negative correlation, adverse market moves are usually more prominent.

Such combinations of various events and their knock-on effects can only be captured and analyzed through a full range of multi-period and multi-dimensional scenarios. None of the outcomes can be chosen as a single prediction. But when analyzed together, we can “predict” the range of feasible outcomes for which an organization should be ready.

The point of the scenario analysis is to predict robust tail risk over a much longer time horizon (more than one quarter); it takes time for banks to take strategic actions and to start changing lending, hedging or funding policies. That’s why it’s important to have early warning signals and contingency planning ahead of time.