Tokenization has the potential to revolutionize markets, primarily through the application of blockchain technology. It allows assets – particularly high-value ones like real estate, art, and company shares – to be divided into smaller, more affordable units. This fractional ownership makes it possible for a larger pool of investors to participate, increasing liquidity and accessibility.

However, there is also a downside to the rise of tokenization. Regulatory and cyber risks, for example, are higher than with traditional assets. Perhaps even more importantly, tokenized assets are expected to attract a wave of retail investors, who are more prone to market panic than their institutional counterparts.

Let’s now take a closer look at the pros and cons of tokenization, starting with the positive.

A Multitude of Benefits

Tokenization can streamline transactions by reducing the need for intermediaries, such as brokers or custodians. This efficiency can lower transaction costs, reduce the time required for settlements and eliminate many traditional barriers to entry.

Blockchain technology, which underpins tokenization, offers a transparent and secure ledger for recording transactions and provides an immutable record of ownership. This transparency helps to reduce fraud and enhance trust among parties.

Tokens can be programmed with smart contracts that automatically execute terms of agreements when predefined conditions are met. This programmability can facilitate more complex transactions and innovative financial products.

This new technology is likely to have a dramatic impact on liquidity by transforming traditionally illiquid assets into more easily tradeable digital tokens. As these tokens can be bought and sold individually, a broader pool of investors can participate, creating more frequent transactions and enhancing liquidity.

Moreover, tokenized assets can be traded on blockchain-based platforms that operate continuously (24 hours a day), unlike traditional markets with limited trading hours. This reduces delays and creates a more dynamic market with a wider range of potential investors, increased demand, automated trading, faster transactions and transparent record keeping.

Ultimately, this could lead to the creation of secondary markets for assets that previously had limited or no trading options – such as private equity, luxury goods, and real estate. Investors, in turn, would be able to sell their tokens without waiting for the asset to mature or be liquidated.

While tokenization could reduce fees in the investment management sector, it compensates by driving higher transaction volumes and individual consumer benefits.

Furthermore, as regulatory frameworks evolve to accommodate tokenized assets, the legal certainty and acceptance of these assets are improving. This regulatory clarity is encouraging more institutional investors to enter this space, adding to the hype.

Given all these potential benefits, it should come as no surprise that analysts predict significant growth in tokenized assets under management.

The Volatility Conundrum

Tokenized assets, however, are also likely to attract more retail investors and will therefore be subject to greater volatility. Unlike institutional investors, who are more likely to hold on to the assets when there is no fundamental reason to liquidate them, retail investors are prone to panic selling – a tendency that has in the past led to market crashes.

Will this increased volatility outweigh the expected gains of tokenization, at least in the medium term? History offers some guidance.

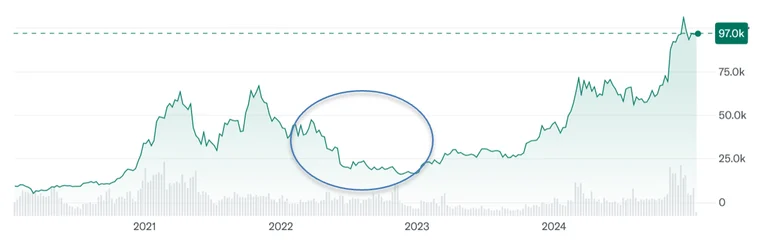

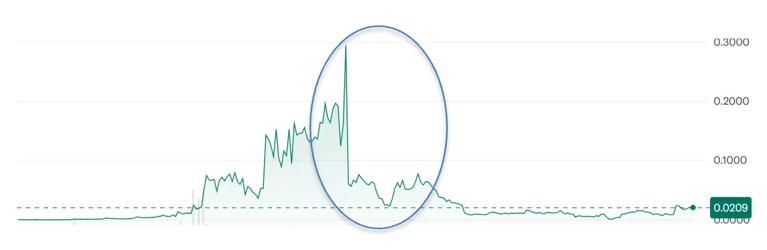

Indeed, we have quite a few examples of extreme volatility in new, fashionable asset classes. Figure 1 illustrates the recent behavioral patterns of Bitcoin and non-fungible tokens (NFT). Both markets crashed in 2022 (see the time periods circled in blue in Figure 1), representing the final shoe to drop before the 2023 demise of Silicon Valley Bank.

High inflation and overheated markets contributed to the downturns of Bitcoin and NFT, as well as to the decline in the broader cryptocurrency market. Cumulatively, these events made risky investments less appealing.

Figure 1: Bitcoin and NFT Volatility

Bitcoin USD (BTC-USD)

Worldwide NFT, Inc. (WNFT)

As always with speculative bubbles, the initial hype led to unsustainable price increase. When a bubble bursts, the assets that were supposed to provide diversification, as observed in stable markets, all crash together. The Bitcoin and NFT downturns were no different.

Similar behavior happened during dotcom crash in the early 2000s, as well as during subprime mortgages meltdown that preceded 2008 global financial crisis (GFC), when all fund-of-funds became highly correlated and went down together.

The exchange-traded fund (ETF) market, which has been around for a while, can serve as a proxy for how tokenization could lead to such bubbles. ETFs are a regulated, diversified financial product based on traditional securities, traded on established markets.

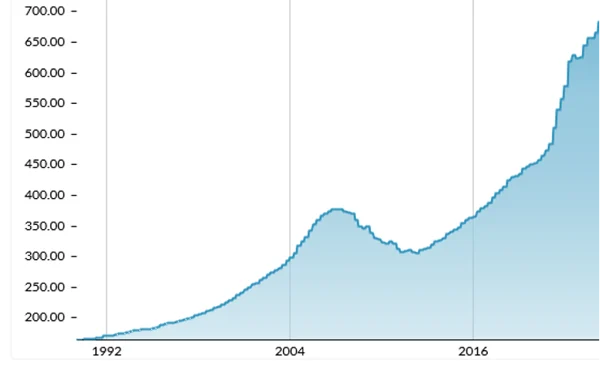

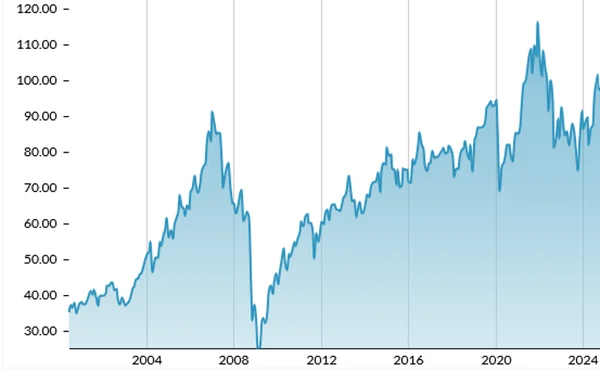

The top panel in Figure 2 (below) shows U.S. house price index for the past three decades. This graph represents real asset transactions for regular (and thus illiquid) real estate values. The bottom panel of Figure 2 shows the performance of iShares U.S. Real Estate ETF (which represents exchange-traded instruments) across the past 20 years. The former have a much smoother performance than the latter, which is highly volatile.

Figure 2: U.S. Real Estate Index vs. Real Estate ETF

All-Transactions House Price Index for the U.S.

The annualized volatility of house price index on the left is 2.83%, with an annualized expected growth rate of 4.22%. The annualized volatility of real estate ETF (bottom panel), on the other hand, is 20.8%, with an expected growth rate of 5.11%.

In highly stressful periods, everything declines – but liquid ETFs show much bigger drops during such times. Consumers investing in ETFs, in short, are much more prone to panic during market stresses. Tokenization would substantially expand the range of assets that would follow the same pattern.

Though there are no historical precedents for tokenization-driven downturns, we can use ETFs to illustrate how firms can anticipate an 80% drop in investment value of tokenized assets over a short time horizon.

Until November 2007, the annual ETF growth rate was more than 13%, with the volatility of less than 16%. But in 2008, amid the GFC, the growth rate quickly bottomed out and volatility spiraled out of control. A standard Monte Carlo (MC) simulation for ETFs would have missed the sharp decline in the ETF assets between November 2007 and March 2009 – by a lot.

How can we better account for such volatility for tokenized assets? The answer lies in introducing various historical and hypothetical shocks that might happen with a certain probability and severity. This interrupts the diffusion process of the standard simulation.

For example, for real estate tokens, applying a shock with 70-80% decline and with the probability of 5% can be justified, because it would capture the real estate ETF worst-case decline as the 99th percentile worst-case outcome.

Parting Thoughts

The hype around tokenization is driven by its potential to fundamentally change how assets are owned, traded and managed. By leveraging the benefits of blockchain technology, tokenization promises greater efficiency, transparency and inclusivity in the financial markets and beyond.

As this technology matures and regulatory environments adapt, the practical applications and advantages of tokenization are likely to become even more pronounced. It can significantly boost liquidity by transforming illiquid assets into highly-liquid instruments – but could also lead to sudden drops in values.

Fully automated, AI-driven trading, which would help smooth market volatility, might take a long time to realize. It’s like self-driving cars – it’ll be a while before they help eliminate accidents on the roads.

But the potential for sudden drops in value of tokenized assets, at times when investors might need liquidity, must be incorporated into strategic asset allocation decision. Full-range scenario analysis incorporates such shocks and respective changes in correlations, while simultaneously assessing capital and liquidity needs and both mark-to-market and cashflow outcomes. It will, moreover, take into consideration risk tolerance, accounting/regulatory constraints and a firm’s specific preferences.

The only way to reap the benefits of tokenization while also being prepared for its potential downsides is to consider the full range of scenarios – including regulatory, cyber and idiosyncratic shocks and their snowball effects.