Equities, bonds and cash. This is the holy trinity of assets where investment managers stash most of their money. They may have a bit of all three; they may invest exclusively in stocks, and then only in “safe” sectors. How they divvy up their allocations will, of course, depend on the amount of risk they’re willing to bear. But this approach can leave money managers with a false sense of security. That’s because the interdependencies between the drivers of risk exposure change dramatically – especially during stressful market conditions, such as those we saw when COVID mushroomed into a pandemic, and economies went into lockdown.

SAFE AS HOUSES

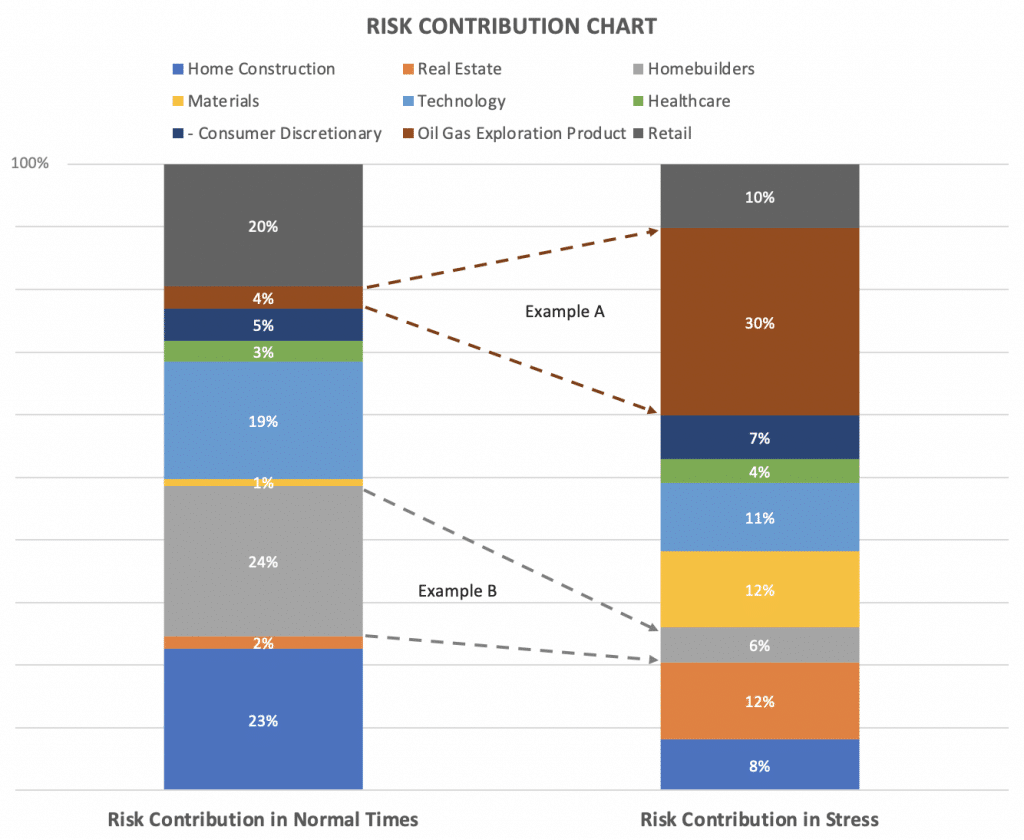

Take a portfolio that allocates its funds equally across a dozen sectors. In this example, when calculating the standard Value-at-Risk (VaR), the largest tranche of risk exposure turns out to be homebuilders; under “normal” conditions (e.g. when markets decline), perhaps one-quarter of your losses will come from this sector; one of the smallest exposures (4%) comes from oil and gas (see chart).

But in stress scenarios, such as the coronavirus pandemic, the situation is very different: here, homebuilders may only account for 6% of your losses; 30% may come from oil and gas (plunging demand as much of the world went into lockdown was exacerbated by a spat between Russia and Saudi Arabia). In other words, there was a hidden risk concentration in a relatively small part of your portfolio. This happens not because homebuilders suddenly became a safe bet during this crisis; rather, oil and gas became much riskier, and thus their proportionate risk contribution increased. Such dramatic shifts in risk allocation happen when investment segments have different behavioral pattern in normal vs stress conditions: low volatility and large jumps in a crisis vs higher volatility but less reaction to crisis

Lesson 1: Hidden risk concentrations must be discovered in advance to assess the readiness for a potential crisis.

BAKED-IN RISKS

Of course, our portfolio manager may have a longer-term outlook, and therefore an appetite for high-risk/high-reward assets, such as private-equity and other alternatives. Yet such investments may end up contributing less to tail exposure than mid-level risk assets, and for very good reason: high-yield exposures like these don’t have much room to deteriorate; their risks are already baked into the investment. You just have to make sure the risk is well covered by additional returns (which wasn’t the case for structured credit in the financial crisis). Contrast this with the mid-level risk assets’ performance, which might deteriorate substantially and unexpectedly. This tail risk isn’t usually covered by their returns.

Lesson 2: High-risk assets aren’t always the ones you need to worry about under a stress scenario.

IT’S ALL ABOUT THAT BASELINE

Crises usually follow a chronology: credit gets crunched, stock markets crash, economies slip into recession and unemployment rises. This time round, though, things happened the other way around: unemployment rose, GDP dropped, markets (briefly) crashed, and credit spreads widened. For that reason, many existing models underestimated the baseline outcome for their portfolios. And so while many banks thought they needed to boost their stress scenarios, they only adjusted their baseline scenarios by 10%-15%. Big mistake! Baseline scenarios often need to be adjusted by 50% or more. Not addressing this issue now might lead to drastic consequences for the financial sector in the future.