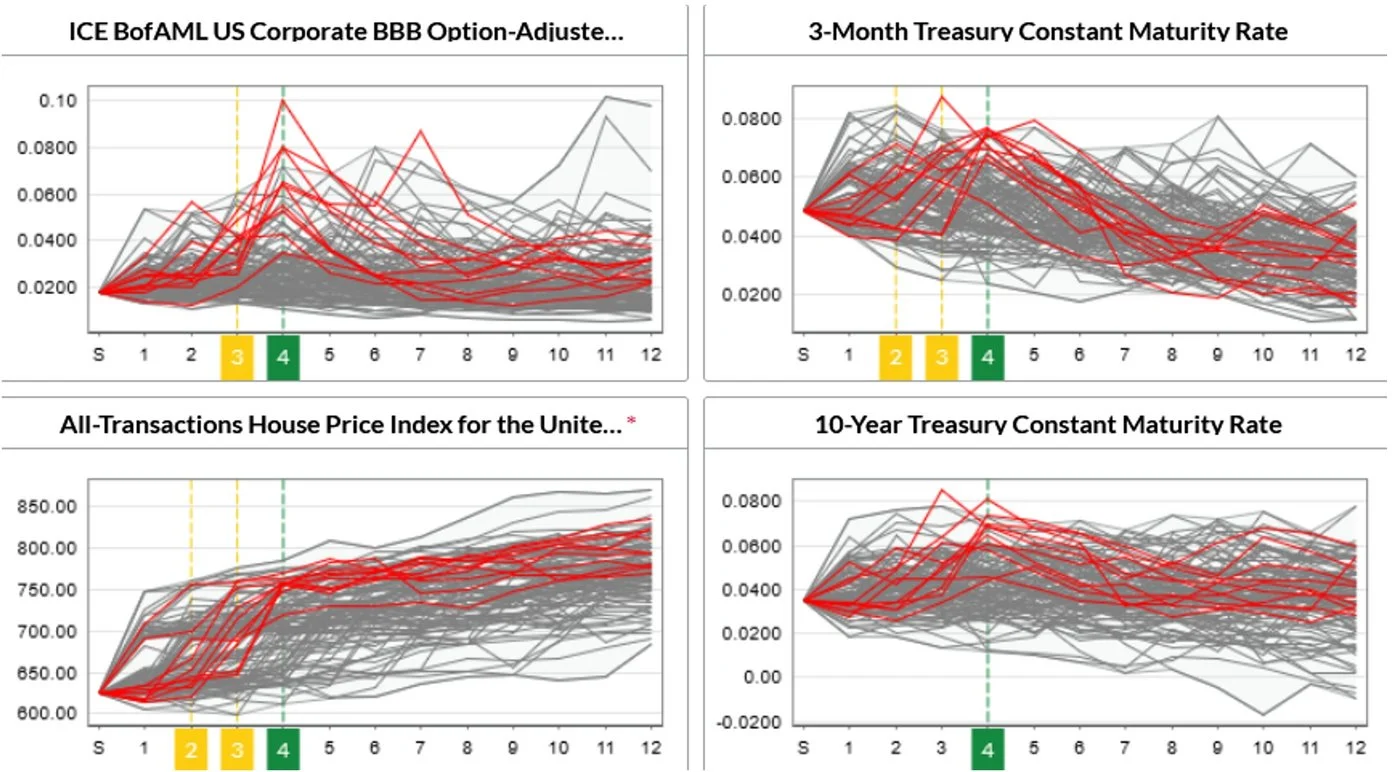

In the interview with Alla Gil, co-founder and CEO of Straterix, the discussion revolves around how banks manage and analyze stress scenarios, emphasizing the traditional three-step process: risk identification, narrative creation, and quantification of impacts. The current method, heavily reliant on past data and modeler’s assumptions, often misses complex market dynamics and lacks early warning signals for proactive action. The introduction of machine learning and stochastic modeling is suggested to automate and enhance the analysis, allowing for a more dynamic understanding of potential outcomes. Artificial intelligence, particularly through machine learning, is highlighted as a key tool for generating synthetic future scenarios and aiding in decision-making by predicting outlier events. Large Language Models (LLMs) are proposed to reverse the traditional stress test sequence, focusing first on data quantification and scenario relevance before narrative construction. The integration of AI and LLMs aims to bolster the banks’ resilience against unexpected market shifts by automating scenario analysis and facilitating adaptive contingency planning. Challenges include the need for a hybrid approach integrating human expert input into AI systems to maintain strategic oversight and ensure sensitive handling of data and predictions.

Interview in Risk.Net with Alla Gil: Enhancing Bank Stress Tests with AI and Advanced Analytics