The past six months have been full of surprises, ranging from the coronavirus pandemic and lockdown, to massive government intervention and soaring stocks.

Against this backdrop, one is almost tempted to feel sorry for risk professionals. After all, it’s their job to make sure senior management is ready for anything – even surprising and unprecedented events. As these put-upon people look to the near future, how can they adapt to the new normal? A good place to start is the future itself.

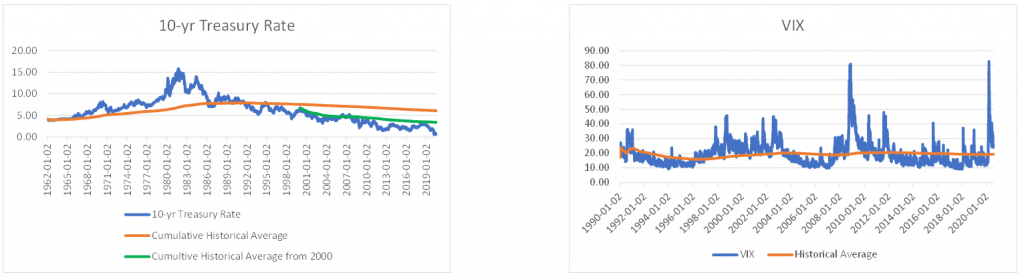

To design future scenarios, one needs to project the trends for related variables. Looking at historical charts for a few critical ones, we see that long-term trends – for the most part – change very slowly. The main outliers are interest rates, which have behaved very differently over the past 20 years, and which now seem to have settled into their own kind of holding pattern. For all other variables, long-term trends have held fairly steady.

So how can we capture unprecedented scenarios based on recent observations? The answer lies in the shocks that affect the variables’ behavior in the scenario. What we’ve seen recently – and have been seeing throughout the history of stress scenarios – is that outliers (variable values far from the trend) should be incorporated into scenario generation by overlaying said shocks, rather than adjusting the trends.

This is how the feedback loop works in this type of the volatile environment. The arrival of new data recalibrates the probability and severity of shocks (trends are adjusted as well, but not materially). Such shock-recalibration must be performed more frequently when we’re in the middle of unfolding stress scenarios, as they are our main means of verification (i.e. they enable us to backtest stress testing). Once the calibration method is validated by backtesting, we can be confident we are indeed ready for any “surprises”.